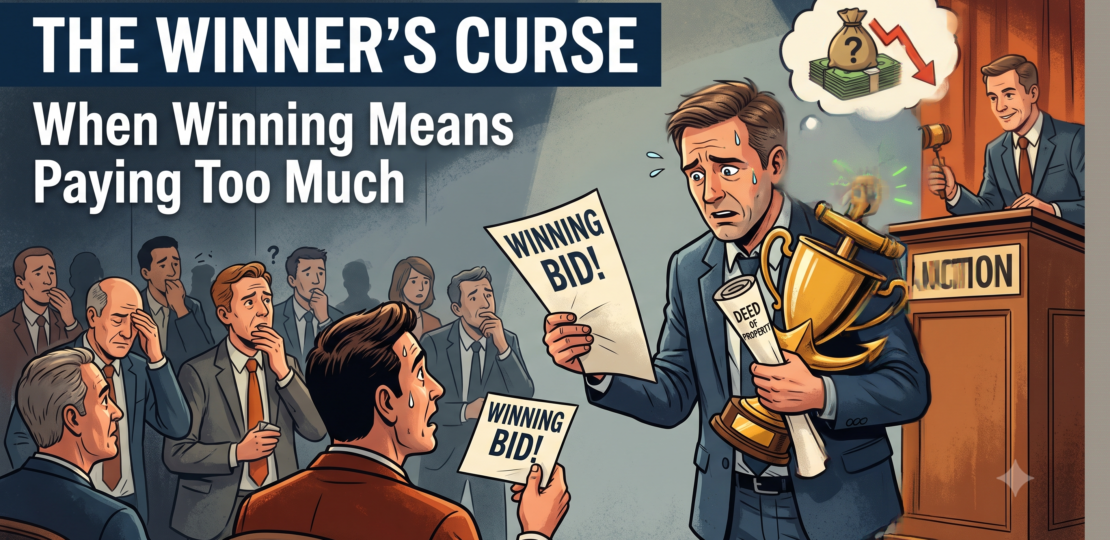

Winning is usually considered the best possible outcome. Whether it is an auction, a competition, or a negotiation, finishing first seems like the obvious goal. Yet economists have long observed situations where the winner is often the one who pays the highest price for being wrong.

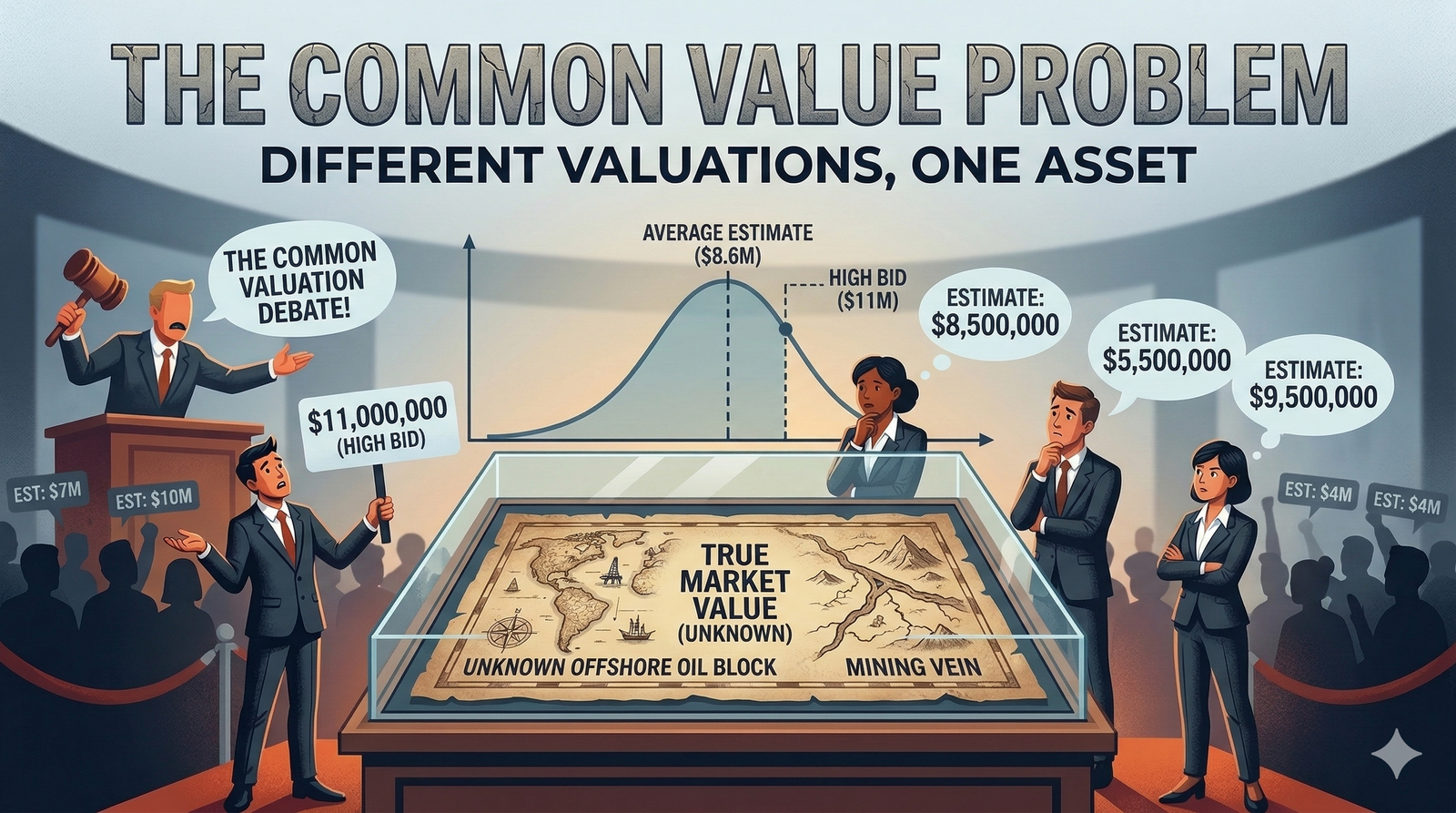

This phenomenon is known as the Winner’s Curse, a concept first introduced by economists Edward Capen, Robert Clapp, and William Campbell in 1971 while studying auctions for offshore oil drilling rights. Companies would independently estimate the value of an oil field before submitting sealed bids. Surprisingly, the companies that won the auctions frequently earned disappointing returns. The reason was simple: the winning bid often belonged to the firm that had made the most optimistic estimate of the field’s value. In other words, winning meant they had likely overestimated what they were buying.

The Winner’s Curse appears whenever many people compete to estimate the value of something whose true worth is uncertain. It has been observed in acquisitions between companies, auctions for artwork, sports contracts, and even online marketplaces. When multiple bidders evaluate the same asset using imperfect information, the highest bidder is statistically more likely to have made the largest estimation error. The more competition there is, the greater the chance that the winning offer exceeds the asset’s actual value.

Rather than discouraging competition, the Winner’s Curse highlights the importance of accounting for uncertainty. Experienced bidders often deliberately bid below their estimated value to compensate for the possibility that they are overly optimistic—a strategy economists call bid shading. The paradox serves as a reminder that success is not determined solely by winning, but by the price paid to achieve it. In markets where information is incomplete, the greatest victory can sometimes belong to the participant who knows when not to win.

RELATED POSTS

View all