Note: This is a continuation of yesterday’s post: The winner’s curse.

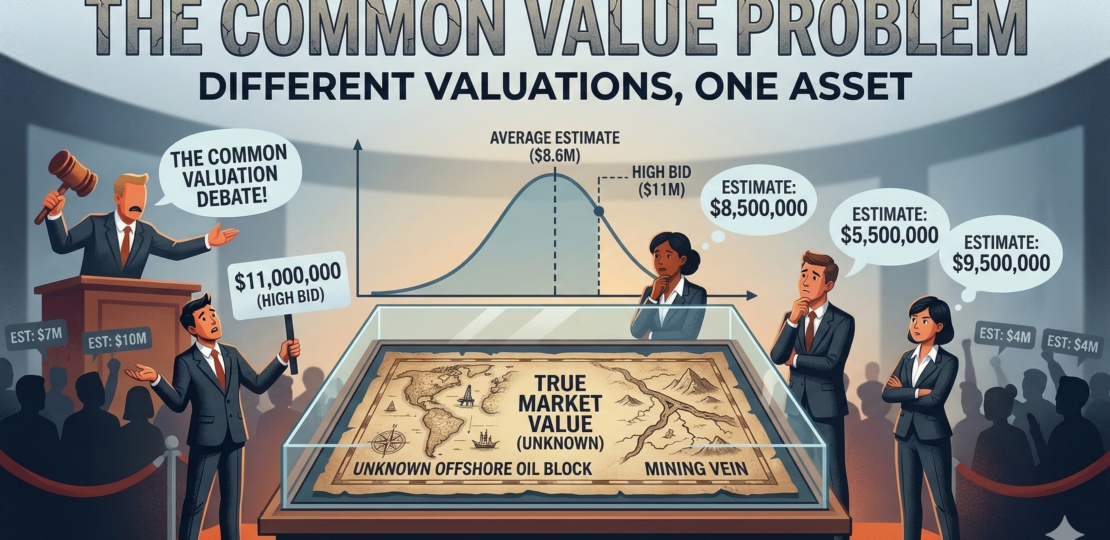

The winner’s curse points to a deeper issue in economics called the Common Value Auction problem. In many markets, the item being sold has roughly the same real value for everyone, but nobody knows that value with certainty.

Take oil fields again. The oil underground doesn’t magically become more valuable depending on who owns it. Its true value is roughly the same for every company. The challenge is that nobody knows the exact amount of oil before drilling begins. Each company must estimate using incomplete data.

Because estimates contain errors, the highest estimate is statistically likely to be an overestimate. If ten analysts independently estimate the same value, the most optimistic one will usually be wrong in the upward direction. Auctions then systematically select the most optimistic guesser as the winner.

This is why experienced bidders focus less on their own estimate and more on what other bidders might be thinking. If many competitors are aggressively bidding, it may signal that everyone’s estimates are inflated. The presence of competition itself becomes information.

This insight reshaped how governments design auctions for things like telecom spectrum and natural resources. Auction formats now try to reveal more information during the bidding process so companies can adjust their expectations before committing to huge payments.

The lesson extends far beyond auctions. In any competitive environment—startup funding, company acquisitions, even housing markets—winning can sometimes mean you were the most optimistic person in the room. And optimism, while admirable in life, can be expensive in markets.

RELATED POSTS

View all